Indian income tax Wikipedia.

1. Penalty under section 271(1)(c)[19] for either concealment of income or for furnishing inaccurate particulars of income:-

Income tax in India

Income Tax in India

Central Revenue collections in 2007-08 (Source: Compiled from reports of Comptroller and Auditor General of India for relevant years)

Personal income tax (direct) (17.43%)

Corporate tax (direct) (33.99%)

Other Taxes (direct) (2.83%)

Excise duty (indirect) (20.84%)

Customs duty (indirect) (17.46%)

Other taxes (indirect) (8.68%)

The Constitution of India → Schedule VII → Union List → Entry 82 has given the power to the Central Government to levy a tax on any income other than agricultural income, which is defined in Section 10(1) of the Income Tax Act, 1961.[1] The Income Tax Law consists of Income Tax Act 1961, Income Tax Rules 1962, Notifications and Circulars issued by Central Board of Direct Taxes (CBDT), Annual Finance Acts and judicial pronouncements by the Supreme Court and High Courts.

The government imposes a tax on taxable income of all persons who are individuals, Hindu Undivided Families (HUF's), companies, firms, LLP, association of persons, body of individuals, local authority and any other artificial juridical person. Levy of tax on a person depends upon his residential status. The CBDT administers the Income Tax Department, which is a part of the Department of Revenue under the Ministry of Finance, Govt. of India. Income tax is a key source of funds that the government uses to fund its activities and serve the public.

History

Ancient Times

Taxation has been one of the key function of the sovereign state since ancient times. In Manusmriti, the Manu, stated that king has the sovereign power to levy and collect tax according to sastras.[4]

In Bodhayana Dharmasutras, it is mentioned that the king got 1/6th part of income from his subjects which was legally termed as tax. In lieu of this tax, the king has a duty to protect his subjects.[4]

According to Kautilya's Arthashastra - an ancient treatise on the study of economics, the art of governance and foreign policy - artha has a much wider significance than wealth. According to him, the power of the government depended upon the strength of its treasury. He states: "From the treasury comes the power of the government, and the earth, whose ornament is the treasury, is acquired by means of the treasury and army." In Raghuvamsh, Kalidas, eulogizing King Dalip, said, "it was only for the good of his subjects that he collected taxes from them just as the sun draws moisture from the earth to give it back a thousand time."[5]

Modern Times

The 19th century saw the establishment of British Rule in India. Following the Mutiny of 1857, the British Government faced an acute financial crisis. To fill up the treasury, the first Income-tax Act was introduced in February, 1860 by James Wilson, who became British-India's first Finance Minister.[5] The Act received the assent of the Governor Generalon July 24, 1860, and came into effect immediately. It was divided into 21 parts consisting of no less than 259 sections. Income was classified under four schedules: i) income from landed property; ii) income from professions and trade; iii) income from securities, annuities and dividends; and iv) income from salaries and pensions. Agricultural income was subject to tax.[5]

Subsequently many laws were brought to streamline income tax laws. For example, Super-Rich Tax was introduced in 1918 and new Income-tax Act was passed in 1918. But most important among all these were the Income-tax Act of 1922. This Act of 1922 marked an important change from the Act of 1918 by shifting the administration of the income tax from the hands of Provincial Government to the Central government. Another remarkable feature of this Act was that the rales were to be enunciated by the annual finance Acts instead of in the basic enactment.[6] Again, new Income-tax Act came in 1939.

Contemporary Times

The 1922 Act was amended not less than twenty nine times between 1939 and 1956. A tax on capital gains was imposed for the first time in 1946, although the concept of ‘capital gains’ has been amended many times by later amendments.[6] In 1956, Mr. Nicholas Kaldor to investigate the Indian Tax System in the light of the revenue requirement of the second five-year plan (1956-1961). He submitted an exhaustive report for a coordinated tax system and therefore,the result was the enactment of several taxation Acts, viz., the wealth-tax Act 1957, the Expenditure-tax Act, 1957 and the Gift-tax Act, 1958.[6]

The Direct Taxes Administration Enquiry Committee, under the Chairmanship of Shri Mahavir Tyagi, submitted its Report on Nov 30, 1959 and the recommendations made therein took shape of the Income Tax Act, 1961. The 1961 Act came in to force with effect from 1st April, 1962 by replacing the Indian Income Tax Act, 1922 which had remained in operation for 40 years. The present law of income tax is governed by the Income Tax Act, 1961, which has 298 sections and 4 schedules and is applicable to whole of India including the state of Jammu and Kashmir.[6]

The"Direct Taxes Code Bill" was tabled in the Parliament on 30 August 2010 by the then Finance Minister to replace the Income Tax Act, 1961 and Wealth Tax Act.[7] The bill, however, could not go through and eventually lapsed after revocation of the Wealth Tax Act in 2015.

Amnesty scheme

Charge to income tax

For the assessment year 2016-17, Individuals earning an income up to ₹2.5 lakh (US$3,600) were exempt from income tax.[9]

About 1% of the national population, called the upper class, fall under the 30% slab. It grew 22% annually on average during 2000-10 to 0.58 million income taxpayers. The middle class, who fall under the 10% and 20% slabs, grew 7% annually on average to 2.78 million income taxpayers.[10]

Agricultural income

Agricultural income is exempt from tax as per section 10(1) of the Act. Section 2(1A) defines agricultural income as:

- Any rent or revenue derived from land, which is situated in India and is used for agricultural purposes.

- Any income derived from such land by agricultural operations including processing of agricultural produce, raised or received as rent-in-kind so as to render it fit for the market or sale of such produce.

- Income attributable to a farm house (subject to some conditions).

- Income derived from saplings or seedlings grown in a nursery.

Income partly agricultural and partly business activities

Income in respect of the below mentioned activities is initially computed as if it is business income and after considering permissible deductions. Thereafter, 40,35 or 25 percent of the income as the case may be, is treated as business income, and the rest is treated as agricultural income.

^a For apportionment of a composite business-cum-agricultural income, other than the above-mentioned, the market value of any agricultural produce, raised by the assessee or received by him as rent-in-kind and utilized as raw material in his business, should be deducted. No further deduction is permissible in respect of any expenditure incurred by the assessee as a cultivator or receiver of rent-in-kind.

Permissible deductions from gross total income

Ministry of Finance has notified certain deductions from gross total income of an assessee. Below are deductions as updated by Finance Act, 2015.

Due date of submission of return

The due date of submission of return shall be ascertained according to section 139(1) of the Act as under:-

If the Income of a Salaried Individual is less than ₹ 500,000 and he has earned income through salary or Interest or both, such Individuals are exempted from filing their Income Tax return provided that such payment has been received after the deduction of TDS and this person has not earned interest more than ₹ 10,000 from all source combined. Such a person should not have changed jobs in the financial year.[12]

CBDT has announced that all individual/HUF taxpayers with income more than ₹ 500,000 are required to file their income tax returns online. However, digital signatures won't be mandatory for such class of taxpayers.[12]

Advance tax

Advance tax is also known as pay as you earn tax as it can be deposited from time to time with the income tax department in advance as opposed to the lump sum amount. The advance tax is to be paid as per the due dates mentioned by the income tax department in the form of installments.

Under this schemes, every assessee is required to pay tax in a particular financial year, preceding the assessment year, on an estimated basis. However, if such estimated tax liability for an individual who is not above 60 years of age at any point of time during the previous year and does not conduct any business in the previous year, and the estimated tax liability is below ₹ 10,000, advance tax will not be payable.

Until FY 2015-16, the due dates and amount of advance tax were different for corporate taxpayers and individual taxpayers.However, from FY 2016-17, both categories of taxpayers were brought at par. Further, individuals opting presumptive scheme of taxation u/s 44AD, 44ADA are liable to pay advance tax in single instalment.

The due dates of payment of advance tax for F.Y 17-18 are:-

Any default in payment of advance tax attracts interest under section 234B and any deferment of advance tax attracts interest under section 234C.

Tax deducted at source (TDS)

The general rule is that the total income of an assessee for the previous year is taxable in the relevant assessment year. However, income tax is recovered from the assessee in the previous year itself by way of TDS. The relevant provisions therein are listed below. (To be used for reference only. The detailed provisions therein are not listed below.1)

^1 At what time tax has to be deducted at source and some other specifications are subject to the above sections.

^2 In most cases, these payments shall not to deducted by an individual or an HUF if books of accounts are not required to be audited under the provisions of the Income Tax Act,1961 in the immediately preceding financial year.

^2 In most cases, these payments shall not to deducted by an individual or an HUF if books of accounts are not required to be audited under the provisions of the Income Tax Act,1961 in the immediately preceding financial year.

In most cases, the tax deducted should be deposited within 7 days from the end of the month in which tax was deducted.

Corporate income tax

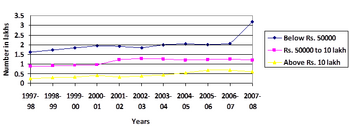

Income-wise number of corporate assessees in India

For Domestic Companies, the tax rate shall be flat 30%. However, as per Finance Act, 2018, the tax rate for MSME has been reduced from 29% to 25% for companies having turnover or gross receipts less than Rs.400 Crores in the last year i.e. in Financial Year 2018-19. Surcharge and Cess shall be levied over and above the flat rate of tax. Therefore, for large corporates, the tax rate is still 30% but for MSME (Micro, Small and Medium Enterprise) it has been reduced to 25%.

For Foreign companies, the tax rate shall be 40% in India for normal income. However, specifically in case of Royalty income or fees for rendering technical services the tax rate shall be 50%. Surcharge and Cess shall be levied over and above the flat rate of tax.[13]

Note - For both companies, an EC and SHEC of 3% (on both the tax and the surcharge) will be payable till F.Y 17-18.But, from F.Y 18-19, the EC and SHEC has been replaced by Health and Education Cess @ 4%.From 2005-06, electronic filing of company returns is mandatory till date.[14]

Surcharge1

Non-corporate assessee: Surcharge of 10 % shall be levied if income is more than 50 lakhs but less than Rs. 1 crore. Further, Surcharge of 15% shall be levied in case the income is more than 1 crore of an individual. Corporate assessee:

^1 Applicable from assessment year 2015-16 onwards.

Tax returns

Categories

There are five categories of income tax returns.

- Normal return u/s 139(1)

Any assessee (Company or firm or a person) who's income exceeds the maximum amount which is not chargeable to tax is required to file return u/s 139(1) within the due date. Currently, the maximum amount not chargeable to tax (basic exemption limit) for individuals is Rs. 2,50,000 for below 60 years, 3,00,000 for 60 years to 79 years and 5,00,000 for 80 years and above. The due date is different for various assessees.

- Belated return u/s 139(4)

In case of failure to file the return on or before the due date, belated return can be filed.As per Budget 2016, it can be filed before the expiry of relevant assessment year.

- Revised return u/s 139(5)

In case of any omission or any wrong statement mentioned in the normal return can be revised.As per Budget 2017, the return can be revised at any time before the expiry of relevant assessment year.Further, from F.Y 16-17, the belated return can also be revised.

- Defective return u/s 139(9)

If the assessing officer considers the return as defective, he may intimate the defect. One has to rectify the defect within a period of fifteen days from the date of such intimation.

- Apart from the above-mentioned categories, the return is also required to filed in response to notices under the various sections like section 142(1)(i), 143(1)(a), 139(9), 154 etc. of the income tax act, 1961.

Statistics

Annual information return and statements

Annual information return

Those who are responsible for registering, or, maintaining books of account or other documents containing a record of any specified financial transaction,[16] shall furnish an annual information return in Form No.61A.

Statements by producers

Producers of a cinematographic film during the financial year shall, prepare and deliver to the Assessing Officer a statement in the Form No.52A,

- within 30 days from the end of such financial year or

- within 30 days from the date of the completion of the production of the film,

whichever is earlier.

Statements by non-resident having a liaison office in India

With effect from 01,June 2011, Non-Resident having a liaison office in India shall prepare and deliver a statement in Form No. 49C to the Assessing Officer within sixty days from the end of such financial year.

Income tax rates for individuals

Income Tax Rates for Financial Year 2017-2018 & Assessment Year 2018-2019

Income Tax Rates Slab for FY 2017-18 (AY 2018-19) - The Finance Bill, 2017

RATES FOR CHARGING INCOME-TAX IN CERTAIN CASES, DEDUCTING INCOME-TAX FROM INCOME CHARGEABLE UNDER THE HEAD "SALARIES" AND COMPUTING "ADVANCE TAX"

In cases in which income-tax has to be charged under sub-section (4) of section 172 of the Income-tax Act or sub-section (2) of section 174 or section 174A or section 175 or sub-section (2) of section 176 of the said Act or deducted from, or paid on, from income chargeable under the head "Salaries" under section 192 of the said Act or in which the "advance tax" payable under Chapter XVII-C of the said Act has to be computed at the rate or rates in force, such income-tax or, as the case may be, "advance tax" [not being "advance tax" in respect of any income chargeable to tax under Chapter XII or Chapter XII-A or income chargeable to tax under section 115JB or section 115JC or Chapter XII-FA or Chapter XII-FB or sub-section (1A) of section 161 or section 164 or section 164A or section 167B of the Income-tax Act at the rates as specified in that Chapter or section or surcharge, wherever applicable, on such "advance tax" in respect of any income chargeable to tax under section 115A or section 115AB or section 115AC or section 115ACA or section 115AD or section 115B or section 115BA or section 115BB or section 115BBA or section 115BBC or section 115BBD or section 115BBDA or section 115BBE or section 115BBF or section 115BBG or section 115E or section 115JB or section 115JC] shall be charged, deducted or computed at the following rate or rates:—

(I) In the case of every individual other than the individual referred to in items (II) and (III) of this Paragraph or Hindu undivided family or association of persons or body of individuals, whether incorporated or not, or every artificial juridical person referred to in sub-clause (vii) of clause (31) of section 2 of the Income-tax Act, not being a case to which any other Paragraph of this Part applies,—

(II) In the case of every individual, being a resident in India, who is of the age of sixty years or more but less than eighty years at any time during the previous year, -

(III) In the case of every individual, being a resident in India, who is of the age of eighty years or more at any time during the previous year, -

Assessments

Self-assessment is done by the assessee himself in his Return of Income. The department assess the tax of an assessee under section 143(3) (scrutiny), 144 (best judgement), 147 and 153A (search and seizure). The notices for such assessments are issued under section 143(2), 148 and 153A respectively. The time limits are prescribed under section 153.[18]

Tax penalties

There are various penalties & fees which can be levied as per the Income Tax Act, 1961. Some of the important penalties and fees are discussed as under :

1. Penalty under section 271(1)(c)[19] for either concealment of income or for furnishing inaccurate particulars of income:-

If the Assessing Officer or the Commissioner (Appeals) or the Commissioner in the course of any proceedings under this Act, is satisfied that any person-

(b) has failed to comply with a notice under sub-section (1) of section 142 or sub-section (2) of section 143 or fails to comply with a direction issued under sub-section (2A) of section 142, or (c) has concealed the particulars of his income or furnished inaccurate particulars of such income,

he may direct that such person shall pay by way of penalty,-

(ii) in the cases referred to in clause (b), in addition to any tax payable by him, a sum of ten thousand rupees for each such failure; (iii) in the cases referred to in clause (c), in addition to any tax payable by him, a sum which shall not be less than, but which shall not exceed three times, the amount of tax sought to be evaded by reason of the concealment of particulars of his income or the furnishing of inaccurate particulars of such income.

In other words, u/s 271(1)(c), the penalty may range from 100 % to 300% of the amount of tax sought to be evaded.

2. Penalty u/s 270A for under reporting or misreporting of income :-

The Assessing Officer or the Commissioner (Appeals) or the Principal Commissioner or Commissioner may direct any person to pay a penalty in addition to tax, if he has under-reported or misreported his income while filing his return.

In case of under reported income, the penalty shall be 50% of the amount of tax payable on under reported income. Further, in case of misreporting income, the penalty shall be 200% of the amount of tax payable on misreported income.

3. Fee u/s 234F for late filing of ITR :-

As per the budget 2017, a new section 234F has been introduced to ensure timely filing of returns of income. According to Section 234F, if a person is required to file income tax return (ITR) as per income tax law (section 139(1)) but does not file it within the due date then late fees shall be levied upon him. The amount of fees shall depend upon the time of filing the return and total income.

The quantum of fees u/s 234F has been enumerated as below : (i) If the return is filed after 31st July but on or before the 31st day of December of the assessment year - Rs. 5000(ii) If the return is filed after 31st December of the assessment year - Rs. 10,000 However, if the Total income is less than or equal to five lakh rupees, then in that case, the fee amount shall not exceed Rs. 1000.

The provisions of this section shall be applicable from in respect of Income Tax returns to be filed for FY 2017-18 (or AY 2018-19).This section shall be applicable on all persons including Individual, HUF, Company, Firm, AOP etc., if the return is filed after their respective due dates.Financial year 17-18 would be the first year when any such fees would be leviable without the intervention of Assessing Officer.

Appeals

When taxpayers dispute the income tax demands raised on them, a structured appeal process has to be followed. The first level of appeals lies with the CIT (A). The next level of appeal lies with the Income Tax Appellate Tribunal - an independent body, which is the final fact finding authority. Courts can subsequently be approached by the aggrieved party only if a question of law is involved.[20][21]

See also

References

- ^ Institute of Chartered Accountants of India (2011). Taxation. ISBN 978-81-8441-290-1.

- ^ "Growth of Income Tax revenue in India" (PDF). Retrieved 16 November2012.

- ^ "Home - Central Board of Direct Taxes, Government of India". Incometaxindia.gov.in. Retrieved 18 April2018.

- ^ a b c Jha S M (1990). “Taxation and Indian Economy”. New Delhi: Deep and Deep Publications.

- ^ a b c "The evolution of income-tax". www.thehindubusinessline.com.

- ^ a b c d "EVOLUTION OF INCOME TAX SYSTEM IN INDIA" (PDF). Shodhganga.

- ^ "Impact of DTC on India Inc", The Hindu Business Line, 6 September 2010

- ^ "Black money haul: Rs 65,250 crore collected through Income Declaration Scheme", The Economic Times, 1 October 2016

- ^ "All you need to know about Income Tax Returns for AY 2016-17", Daily News and Analysis, 16 April 2016

- ^ Santosh Tiwari. "Evasion of personal tax dips to 59% of mop-up". The Financial Express.

- ^https://www.incometaxindia.gov.in/pages/acts/income-tax-act.aspx

- ^ a b "E-Filing is mandatory Income is more than 5 lacs". CA club india.

- ^ "Income Tax rates for Companies". businesssetup.in.

- ^ Corporate taxpayers must file electronically, point 4 of I T circular.

- ^ "e-Filing Statistics", incometaxindiaefiling.gov.in

- ^ "Annual Information return".

- ^ Kumar, Pawan. "Income Tax Rates Slab for FY 2017-18 (AY 2018-19) - Param News: Latest India News, Breaking News, Sports, Bollywood, Politics, Jobs". www.paramnews.com. Retrieved 20 April 2017.

- ^ "Readers' Corner: Taxation", Business Standard, 27 March 2016

- ^ Section 271 of India IT Act

- ^ "CIT (Appeals) to pass orders within a fortnight", The Times of India, 23 June 2015

- ^ Income Tax Deductions Under Section 80 to save Tax

Comments

Post a Comment

jarvisshukla123@gmail.com